Navigating New Jersey’s Auto Insurance Requirements: A Beginner’s Guide

Navigating the complexities of auto insurance requirements can be daunting for newcomers in New Jersey. This guide aims to simplify the process and provide you with a clear understanding of the state’s insurance mandates. Whether you are a new resident or a first-time car owner, it’s crucial to comprehend the coverage levels necessary to stay protected and legally compliant on the road. In the following sections, we will dissect the different types of insurance, minimum coverage amounts, and additional options that could provide the peace of mind you need as you travel the Garden State’s highways and byways.

Understanding New Jersey’s Auto Insurance Requirements

Minimum Liability Coverage Limits

In New Jersey, drivers are legally required to carry liability insurance to cover damages or injuries they may cause to others in an accident. The minimum liability coverage limits are as follows: $15,000 for bodily injury per person, $30,000 for total bodily injury per accident, and $5,000 for property damage per accident. These minimum limits are often referred to as 15/30/5 coverage.

Personal Injury Protection (PIP) Requirements

Personal Injury Protection, also known as PIP, is mandatory in New Jersey and covers medical expenses for you and your passengers regardless of who is at fault in an accident. The basic PIP coverage amount is $15,000 per person, per accident, but you have the option to choose higher limits.

Uninsured/Underinsured Motorist Coverage

Uninsured/Underinsured Motorist Coverage (UM/UIM) is another essential component of New Jersey’s auto insurance requirements. This coverage protects you if you’re in an accident with a driver who either lacks sufficient insurance or has no insurance at all. The minimum UM/UIM coverage limits tend to mirror the liability limits, providing you with $15,000 for bodily injury per person, $30,000 for total bodily injury per accident, and $5,000 for property damage, although higher limits can be purchased for greater protection.

Factors Affecting Auto Insurance Rates in New Jersey

Factors that influence the cost of auto insurance premiums in New Jersey are diverse and can significantly impact the amount you pay. Among these factors are:

- Demographics: Your age, gender, and marital status can affect your insurance rates. Younger drivers typically face higher premiums due to their lack of driving experience, while married couples may receive lower rates.

- Vehicle Type: The make, model, and age of your vehicle play a crucial role in determining your insurance costs. High-performance vehicles or cars with expensive replacement parts can lead to higher premiums.

- Driving Record: A clean driving record is key to affordable insurance rates. Accidents, traffic violations, and DUI/DWI offenses will likely increase your premium.

- Credit History: Insurance companies often consider credit scores when setting rates. A higher credit score may result in lower insurance costs, reflecting financial stability and responsibility.

- Coverage Options: Opting for higher coverage limits or additional protection like comprehensive and collision coverage will naturally raise your insurance premium, but provide more extensive coverage in the event of an accident.

Understanding these factors can help you make informed decisions about your auto insurance and manage your costs effectively.

Ways to Save on Auto Insurance in New Jersey

When looking to save on auto insurance in New Jersey, comparison shopping is an invaluable strategy. Do not hesitate to obtain quotes from multiple insurance providers to secure the best rate that aligns with your coverage needs. Additionally, many insurance companies offer a variety of discounts which can significantly reduce your premiums. Common discounts include:

- Safety Features: If your vehicle is equipped with safety features such as anti-lock brakes, airbags, and anti-theft devices, you may be eligible for discounts.

- Good Driver Discounts: Maintaining a clean driving record without accidents or traffic violations can earn you a good driver discount.

- Multi-Policy Discounts: Bundling your auto insurance with other policies like homeowners or renters insurance can lead to savings on both policies.

Another effective means of lowering your insurance costs is completing a defensive driving course. Besides sharpening your driving skills, these courses can provide discounts on your insurance premiums upon completion.

Lastly, usage-based insurance programs have become increasingly popular. These programs track your driving behavior through a mobile app or plug-in device, potentially offering discounts for safe driving habits and reduced mileage. It’s worth exploring these programs if you’re comfortable with the monitoring of your driving patterns for potential savings.

By exploring these saving avenues, you can tailor your auto insurance to fit your budget without compromising crucial coverage.

Special Considerations for New Jersey Drivers

No-Fault Insurance System in New Jersey

New Jersey operates under a no-fault insurance system, meaning that after an accident, drivers and passengers utilize their own Personal Injury Protection (PIP) coverage to pay for medical expenses, regardless of which party is at fault. It’s important to understand that this system limits the right to sue the at-fault party unless the case involves severe injuries or death. Therefore, it’s crucial to select an appropriate PIP coverage that sufficiently covers potential medical costs following an accident.

Laws and Regulations Unique to New Jersey

In New Jersey, one of the unique regulations is the choice no-fault law, which permits drivers to choose between a standard policy that maintains the right to sue for any injury, or a basic “limited right to sue” policy, which limits the ability to seek compensation for pain and suffering unless the injuries are catastrophic. Additionally, New Jersey law requires all drivers to maintain liability insurance, PIP, and UM/UIM coverage, which is not the case in all states.

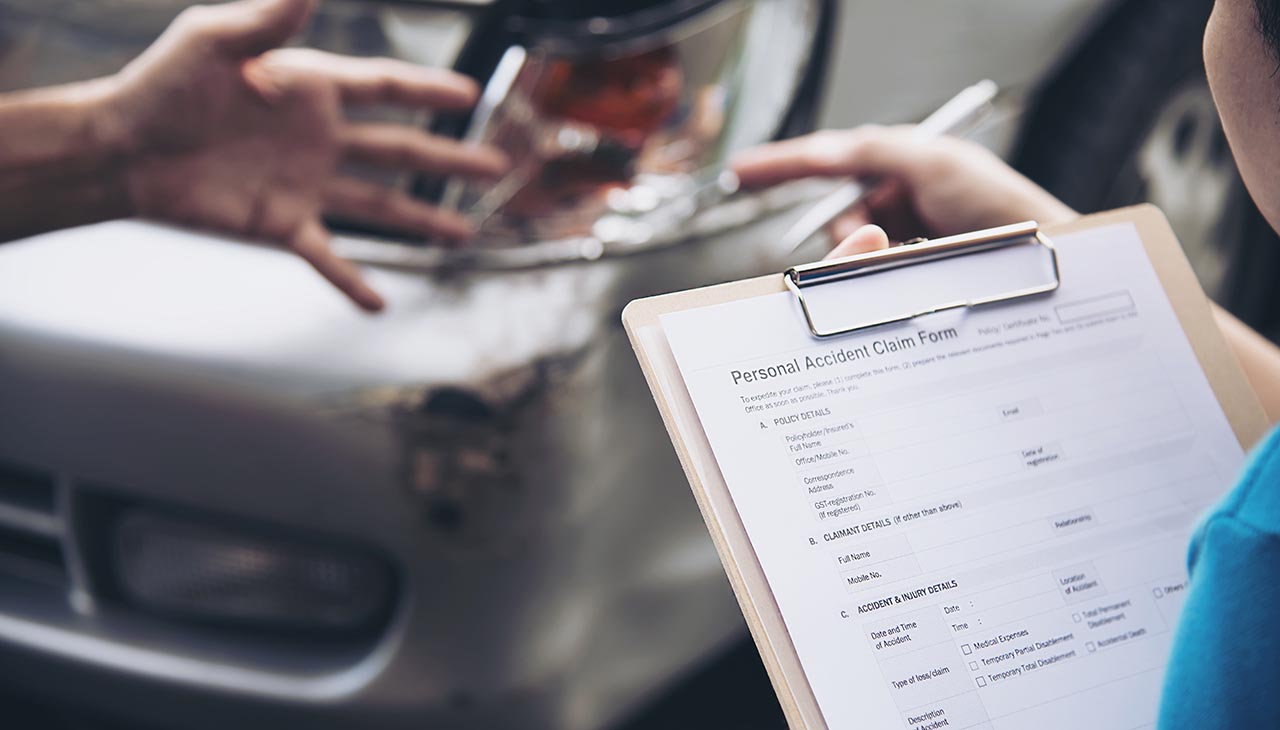

Best Practices for Filing Auto Insurance Claims in New Jersey

For drivers in New Jersey, the best practice when filing an auto insurance claim starts with notifying the insurance provider as soon as possible after an accident. Documenting the scene with photographs, gathering witness statements, and obtaining a copy of the police report will aid in the claims process. It’s also advisable to keep meticulous records of all medical visits and treatments related to the accident as this will facilitate the use of your PIP coverage. Cooperation with your insurance adjuster and understanding your policy’s terms will ensure that the claims process is as smooth as possible.